Update: Non-Covered Benefit Legislation

Part of developing a treatment plan is computing the cost of treatment. During this process, you should determine the portion that will be covered by the patient’s insurance plan, the portion the patient will pay out-of-pocket, and the portion that the practice will be required to write off, when applicable. It is critical to understand the unique requirements and limitations of each patient’s dental plan(s). You must also consider any non-covered benefit legislation that may or may not exist in your state to properly determine the fee that can be received for the service.

To better understand why this issue is so important to a dental practice, let us examine what non-covered services legislation involves and what it means for dental practices.

What Are Non-Covered Services?

The American Dental Association (ADA) defines a covered service as, “Services for which payment is provided under the terms of the dental benefit contract.” Therefore, based on the ADA definition, non-covered services are specific services not reimbursed under the terms of the dental benefit contract.

Most dentists participate in one or more dental networks. As a participating or network doctor, the dentist is typically obligated to accept the network’s predetermined or negotiated fee schedule as payment in full for the services provided, regardless of the practice’s actual fee for the service. The participating dentist is then contractually obligated to write off any amount that exceeds the network’s allowable fee schedule.

In the past, some dental networks have allowed participating providers to bill their full fee for a service not covered by a patient’s dental plan. Others have restricted participating dentists to their network fees even when services were not covered. Some plans grandfathered dentists who had older participating provider contracts, allowing them to charge their full fees for non-covered services, but restricted newer participating providers to their network fees. When a payer requires that the practice accept a predetermined fee for a service that is not covered under the plan, it is referred to as “fee capping” for non-covered services.

Due to the continuing financial impact of today’s sluggish economy and increasing overhead costs, many dentists question why they should be restricted to network fees for services that are not covered by dental plans. It is with this mindset that we turn our attention to the legislative battles over non-covered services that have erupted across the country over the past decade.

A Little Bit of History

In 2008, the Delta Dental Plans Association (DDPA) announced plans would require all Delta Dental participating providers to honor locally approved Delta Dental fees, even for non-covered services, by January 2011. Up to this point, some Delta Dental payers had allowed participating providers to charge their full fees for non-covered services, including those services performed after the patient’s maximum benefits had been reached. DDPA’s goal was to standardize Delta Dental contract provisions throughout the country. Although several national dental payers had been restricting fees for non-covered services for several years, Delta Dental’s announcement was the final straw that prompted several state dental associations to take action and initiate noncovered services legislation.

Non-Covered Services Legislation

Many dental professionals and organizations share the belief that it is unreasonable for a payer to require a dentist to accept a reduced, negotiated fee when the payer has no financial responsibility for it. This is especially true for major services where the predetermined fee may not even cover the cost of the procedure provided. Some even feel that this fee capping could deter dentists from participating in some networks. A lack of participation, especially in rural, underserved areas, could further limit patients’ access to care.

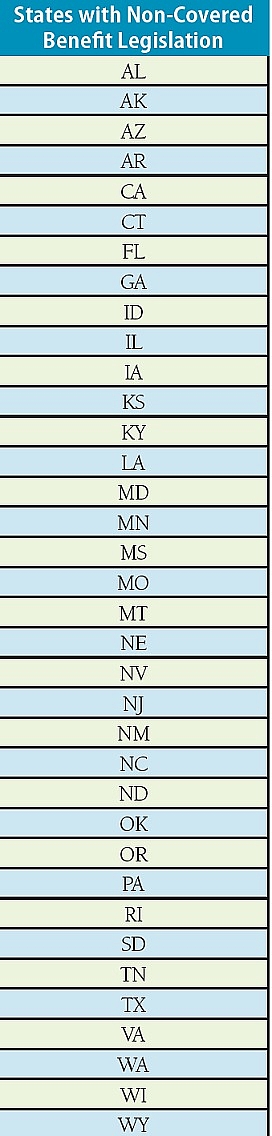

This shared sentiment has led many states to propose and pass legislation preventing fee capping of non-covered services. To date, 36 states have adopted various forms of non-covered services legislation (see list on page 9). There is a great deal of contention surrounding this issue, but of the legislative bills that have passed, most have done so by a wide margin. In fact, as of this writing, only one state (Colorado) has failed to pass its proposed non-covered services legislation, and that bill failed with a tied vote.

Federal Plans and Self-Funded ERISA Plans

It is important to remember that federal dental plans are not subject to state insurance laws, but are governed by federal law. Therefore, any non-covered services legislation ratified by a state may not apply to dental plans that cover federal government employees (i.e., FEDVIP plans), dependents of active duty military (i.e., TRICARE), or other types of federal plans.

In addition, self-funded dental plans are regulated by the Employee Retirement and Income Security Act of 1974 (ERISA), and are exempt from state insurance laws. This type of plan is common with large employer groups, unions, government employers, etc. and are often managed by insurance companies serving as third-party administrators (TPA). Furthermore, while only about 25 percent of insured patients are covered by traditional “insured” plans subject to state law, about 75 percent of insured patients are covered by self-funded plans that are governed by federal ERISA Following the success of state legislation, a bill has now been introduced in Congress for federal fee capping legislation. On July 29, 2015, Representative Buddy Carter of Georgia introduced HR 3323, better known as the Dental and Optometric Care Access (DOC) Act. In response to the proposed DOC Act, Congress has assigned a committee to further investigate it.

This Act is supported and backed by many healthcare organizations, including the ADA. However, convincing Congress to amend ERISA to allow dentists to charge full fees for non-covered services could be challenging. Getting a federal fee capping law passed would be a huge victory for dentistry, and could be critical to the financial health of dental practices that are struggling to remain financially viable in today’s PPO-controlled environment.

Legislation Details

As previously mentioned, 36 states have passed laws prohibiting fee capping for non-covered services. This means that dental payers cannot limit participating providers’ fees for those services that are not covered by the plan. Therefore, dentists in those states have the right to charge their full practice fee for procedures that are non-covered services. Each of the laws adopted thus far have similar intentions, and contain language similar to the following:

No contract between a dental plan and a dentist for the provision of services to patients may require that a dentist provide services to covered individuals at a fee set by the plan unless said services are covered services under the applicable subscriber agreement.

Simply put, if the payer does not cover a service, the payer cannot mandate what the doctor can charge for that service. However, there are some variations in each state’s exact definition of “covered services,” which can affect the application of the law. Each state’s statutory definition of what it considers to be a covered service delineates when network fees apply and when they do not. Many states have similar definitions, and contain language similar to the following:

Covered services are dental services that are reimbursable (or reimbursement is available) under the plan, but may be subject to patient deductibles or copayments, waiting periods, frequency limitations, plan maximums, alternate benefit payments, or other similar contractual limitations.

To date, Iowa’s legislation is the most favorable for dentists. Iowa’s law defines covered services as, “services reimbursed under the plan.” Therefore, Iowa interprets “covered services” as those services that are paid rather than those that are payable. In Iowa, if a plan pays nothing for the service provided (even if the plan would have covered the service if the patient had satisfied a waiting period or had not exhausted the plan maximum), the dentist is not restricted to the plan’s fee schedule for that service.

This is subtle, but think about how the term reimbursed differs from reimbursable. Reimbursed, simply defined, means paid for. Aside from Iowa, all the other states’ definitions of covered services are more limiting to dentists. Other states typically define covered services in such a way that if the procedure is normally covered by the plan under any circumstances, it is a covered service. Some payers interpret this to mean that a crown performed for cosmetic reasons, rather than restorative reasons, is still considered a covered service, even though it will not be paid by the dental plan.

Minimal Level of Reimbursement Loophole

Virginia had one of the most challenging non-covered services legislation battles. Payers spent a considerable amount of time, money, and energy trying to defeat the legislation. In the end, the Virginia Dental Association and its member dentists prevailed, and the legislation passed.

Although the Virginia law passed and defines a “covered service,” it does not address the issue of the “level of reimbursement.” As a result, some Virginia-based dental plans now reimburse major services at only five percent. For example, a crown ($1,000 fee) performed for cosmetic purposes could be reimbursed at five percent ($50), and leave the dentist unable to balance bill the patient. These payers are able to provide this reduced level of reimbursement because there is no restrictive clause in the state’s noncovered services law, thus the payer can still control fees by offering only minimal reimbursement. The participating dentist is obligated to accept the plan’s fee schedule for that procedure as if the plan has covered the service at 100 percent.

Covering services at a one to five percent reimbursement rate essentially converts a conventional dental benefit plan into a discount plan for the dentists who participate. Unfortunately, none of the non-covered service laws adopted to date have included a clause establishing a minimal level of reimbursement to qualify a procedure as a covered service. Therefore, this trend could occur in states other than Virginia.

For this reason, there are concerns that payers may react to fee capping legislation by adopting a strategy of covering all services at a nominal, or de minimus, fee. This type of strategy is in direct contrast to the spirit and intent of this type of legislation. To combat this, states could consider setting a payment threshold that establishes a fair reimbursement (e.g., 50 percent of the full practice fee).